Essential IRS Compliance of Form 1099-MISC and 1099-NEC for HOAs and Condos Explained

Why is Form 1099 So Important?

Your condo or HOA hired a lot of vendors and made plenty of disbursements this past year. These vendors were not employees of the association, yet were paid substantial sums of money over the course of the year for the goods and services they provided. The IRS requires that businesses, even “not for profit” businesses such as condominium associations and HOAs, to provide a record of the monies paid by the business to these vendors by using one variation or another of Form 1099. It’s not just a suggestion; it’s the law! Additionally, depending on what other items the association has paid for, Form 1099 expenses can offset the amount of tax a condominium association or HOA owes.

For homeowner associations (HOAs) and condominium communities, understanding and complying with IRS regulations, including filing Form 1099 for vendors and other income sources, is crucial. This guide outlines who needs Form 1099, why compliance is essential, and how to manage the process effectively.

Form 1099 is an IRS document that independent contractors receive to report their income from specific sources during the tax year. It’s important to note that these contractors are considered self-employed and not employees of the association.

Types of Form 1099 Relevant to HOAs

- Form 1099-NEC: Used for reporting nonemployee compensation, such as payments to contractors and service providers.

- Form 1099-MISC: Essential for reporting various payments, including those for services rendered and other business-related transactions.

- Form 1099-INT (Investment Interest Income): HOAs may also need to issue Form 1099-INT to report investment interest income earned. This includes interest earned from investments held by the association, such as interest on reserve funds or other financial assets.

1099-MISC vs. 1099-NEC: What Sets Them Apart?

Form 1099-MISC (miscellaneous) is the most familiar form of 1099 that most condo and homeowners’ associations have used in the past. As of 2020, there is a new kid on the block – the1099-NEC (non-employee compensation) form. The new form is used to report self-employment income while the 1099-MISC form is now used to report miscellaneous income such as rent or payments to an attorney. Any expenditures greater than $600 in a calendar year should be reported on a Form 1099 in accordance with IRS rules.

Who Requires Form 1099?

Form 1099 should be issued to individuals or entities that receive $600 or more in non-employment income during the tax year. This includes professional service providers, independent contractors, and those receiving investment interest income.

Entities Generally Not Requiring Form 1099

- Corporations (except for certain payments like attorney fees and medical payments).

- LLCs taxed as Corporations.

- Tax-exempt Organizations under section 501(c) of the IRS Code.

- Government Agencies.

- Payments made by credit card, debit card, gift card, or through third-party payment networks (handled by the payment network).

- Utility companies.

- Rent payments to real estate agents or property managers.

When to Issue a 1099?

HOAs must issue Form 1099 to recipients by January 31 each year for non-employment income over $600, except for certain types like royalties, which typically do not apply to the vast majority of communities. This form is crucial for reporting payments such as royalties and broker payments. Community Financial will ensure compliance by sending the Form 1099-MISC to the vendor, the state, and the federal government for payments made during the year.

What Do I Need to Prepare Form 1099?

Accurate recordkeeping is paramount to accurate 1099 preparation. The IRS requires the filer of the 1099 to provide the Taxpayer Identification Number (TIN) for anyone that is to receive a 1099. A best practice is to require that a payee furnish their TIN (often requiring a W-9 with TIN and mailing address) to the payor prior to payment being issued (and updating the accounting system). The more payees, the more records the association must keep. Additionally, vendors that are corporations do not typically have to be reported when filing 1099s. If a condominium or HOA has engaged the services of a management company and that company is issuing payments, they would also incur the burden of filing the 1099s. As you can see, the whole matter can be quite “taxing” if you’ll pardon the pun.

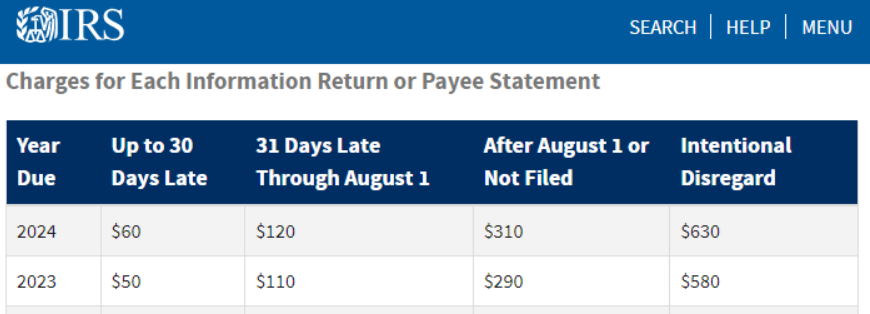

The condo or HOA can also be subject to penalties for several reasons: failure to file timely, missing information or incorrect information. The penalties start at $50.00 and can go as high as $280.00 per form. The penalty amounts change depending on the date of filing. It is important to remember that 1099 filings are due by January 31st to the vendor and February 28th to the IRS.

Late Payment Penalties and Interest

Penalties are applied for each information return that is not filed correctly or on time, as well as for each payee statement that is not provided.

Interest on penalties begins accruing on different dates depending on the penalty amount and type. Interest continues to accrue until your balance is fully paid. For more details on the interest rates we apply, see Interest on Penalties.

Why It’s Important

Failing to file accurate 1099s by the January 31st deadline can lead to significant IRS penalties for HOAs and condo associations. These penalties underscore the importance of meticulous compliance with IRS reporting requirements.

Outsourcing Your Bookkeeping is a Smart Move

For many associations, it just makes sense to outsource this work. Recordkeeping and issuing year-end 1099s without expert help can just be plain tricky. Simple mistakes can cause the association to be outside of compliance and/or miss opportunities to offset their revenue, which can increase their tax burden. Using an outsourced HOA and condominium association record and bookkeeping service like Community Financials is one way to make sure your condominium association or HOA’s 1099s are filed accurately and timely. It reduces risk and can help the association save money.

How Community Financials Can Help

Community Financials offers a comprehensive solution to facilitate compliance with IRS regulations by managing vendor information and overseeing 1099 filings. This helps HOAs and condo associations mitigate the risk of fines and penalties. Stay compliant and utilize our resources to streamline this process efficiently. For more information on how Community Financials can assist your community with accounting, including 1099 compliance, we invite you to fill out our confidential online request for a quote form.